VPPs as the Solution to Data Center Speed to Power

Three residential energy asset providers just made the largest capacity offer in Virtual Power Plant history.

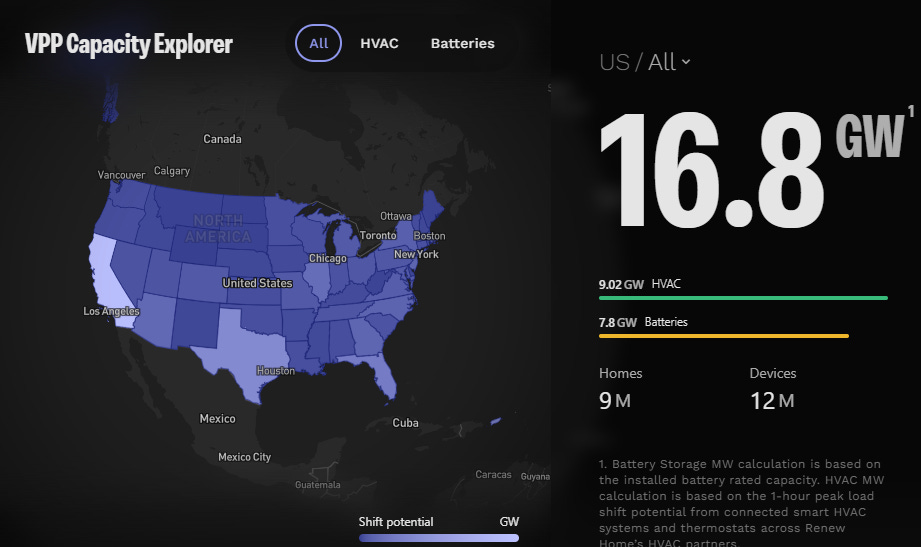

Last week, Renew Home, Sunrun, and Tesla, announced an agreement to make available 16.8 gigawatts of virtual power plant capacity directly to utilities, hyperscalers, the PJM’s reliability backstop process, and first-come first serve interested parties. They are calling it a “Capacity-as-a-Solution framework”. A data center that could otherwise spend several years in the PJM interconnection queue could theoretically have capacity under contract before its next board meeting.

To put 16.8 gigawatts in terms most people can understand, 1 megawatt can power roughly 800 homes (considering regional differences in electricity usage patterns and average home size). On that basis, 16.8 gigawatts represent enough capacity to serve roughly 13.4 million homes, or roughly twice every household in New York City, Los Angeles, and Chicago combined. That comparison is about the massive scale of this partnership based virtual power plant. Caveat, virtual power plant resources typically dispatch for two to four hours at a time, not continuously to replace baseload. Nevertheless, the distributed energy assets are real, already installed, and growing at a healthy pace every day. Sunrun has been at least doubling their VPP megawatts under management at year over year recently. Nor do data centers need VPPs to replace their baseload power. The play is using VPP dispatch to maintain operations during grid stress events when utilities would otherwise ask data centers to curtail.

WHY MEGAWATTS MATTER

A megawatt (MW) is 1,000 kilowatts. Based on EIA data, 1 MW can serve roughly 800 average U.S. homes when running continuously. A gigawatt (GW) is 1,000 megawatts, or enough for about 800,000 homes. A single large nuclear reactor produces roughly 1 GW. The 16.8 GW in this announcement is the nameplate capacity of nearly 17 nuclear reactors, except instead of one central power plant, it is distributed across millions of homes, thermostats, and batteries in every major U.S. power market.

Speed to power has become the defining constraint in data center development, that’s why there are new well-funded startups like GridCARE, who recently raised a $64 million Series A in May 2026 with a core mission is to solve the speed to power issue. Hyperscalers are committing capital faster than generation developers can build the infrastructure to serve it. In Northern Virginia, the densest data center market in the world, Dominion Energy has a backlog of large-load interconnection requests it cannot serve on existing infrastructure. PJM released a backstop procurement framework in April to procure 14.9 gigawatts of new power for large loads by 2031, roughly the output of 15 nuclear reactors, an acknowledgment that the grid does not have headroom for the data center pipeline.

The combined 16.8 gigawatts come from two fundamentally different products. Roughly 54%, about 9 gigawatts, is Renew Home’s demand response network: more than 8.6 million homes of 11 million enrolled smart thermostats and connected devices that can reduce consumption within seconds of a dispatch signal. These are load curtailment assets.

The remaining 7.8 gigawatts comes from Sunrun and Tesla’s battery systems, which can actively export electricity onto the grid during high-stress periods or on a daily passive schedule. If we’re talking a Tesla Powerwall 3, which the majority of the batteries are, then every single of these 1.2 million batteries can move about 11.5 kW each back on to the grid simultaneously.

The capacity is geographically distributed across every major power market in the country, according to vppcapacity.com, which contains an interactive map to drill into each state plus D.C and Puerto Rico. California holds the largest concentration at 4,660 MW, enough to serve roughly 3.7 million homes simultaneously, more residential households than the entire state of Colorado. Texas sits at 1,730 MW, roughly the residential electricity load of the Dallas-Fort Worth metro area, and the second-largest data center market in the country. Puerto Rico ranks third at 1,540 MW, nearly all of it battery storage deployed after Hurricane Maria for residential resilience. That capacity operates on an isolated grid and serves a different purpose than the mainland programs discussed here, it’s included in the dataset but likely is not part of the BYOC framework available to continental data center operators. Virginia shows 313 MW available today, equivalent to the residential load of roughly 250,000 homes, more than twice the size of Richmond, Virginia’s entire customer base, with a committed path to 500 MW by 2030.

WHAT 300 MW MEANS FOR A DATA CENTER

A single large hyperscale data center campus typically draws between 100 and 500 MW of power. The 313 MW Renew Home, Sunrun, and Tesla have available in Virginia today is, on nameplate, roughly equivalent to one full large-campus power draw. That comparison illustrates the immediate commercial opportunity in the state, but also the gap: Virginia alone has many active data center campuses.

Virginia is where the commercial case is sharpest. Loudoun County alone hosts more than 130 data centers, and Dominion Energy’s queue of large-load requests has become one of the most-watched constraints in the power industry. The state passed a first-of-a-kind law this year directing Dominion and Appalachian Power to quantify and reduce grid waste through distributed energy resources.

The commercial structure has a precedent. Voltus introduced it as “bring your own capacity” last fall. The model is a hyperscaler contracts VPP capacity from distributed resources near its data center, the utility calls on those resources during high demand events, and the data center avoids curtailment to its own GPU workloads and operations. Voltus signed its first major deal under this framework with Google a month ago in June, a 100-megawatt contract in PJM, roughly the load of a mid-size data center campus. Renew Home, Sunrun, and Tesla are announcing open for business at 168 times that scale. I view this as one of the most consequential market signals VPPs have ever generated.

Now that hyperscalers are beginning to treat DER portfolios as part of their capacity procurement stack rather than a supplemental curtailment program, the economics of the whole system shift. The value of the megawatts from VPP portfolios may change dramatically. Traditionally VPP’s earn revenue from participating in utility, state-sponsored, or ISO programs that help the grid in times of stress. Think CAISO’s DSGS and ELRP programs, ERCOT’s ADER, National Grid’s ConnectedSolutions program, or any of the ISO’s energy or capacity markets. Those were the default places to deploy managed megawatts historically, but I believe this will shift pretty quickly as more and more supply agreements are reached with data center operators.

In Voltus’s BYOC Google press release they stated “Through this initial deal, Google and Voltus aim to create an industry-leading scalable blueprint for how data center capacity needs can be met affordably and reliably through smarter utilization of the grid. By proving this can be a valuable tool for ambitious data center load growth, the partnership establishes a repeatable path for other large energy users to follow – accelerating clean capacity deployment, bringing direct economic benefits to local communities, and contributing to a robust, reliable grid for everyone.” I believe this framework is exactly what Renew Home, Sunrun, and Tesla are trying to follow and personally I’m very excited to see where this leads for the future of VPPs.

The residential DER build-out that VPP practitioners assembled over the last decade, one battery and one enrolled thermostat at a time, just became the largest power offer in the country. The announcement tells us that the supply exists, and I believe the power-hungry market participants will respond quickly to take advantage of that supply.

Thanks for reading! I also combed through and pulled together the state by state, plus District of Columbia and Puerto Rico data so you don’t have to.

Sources

Household electricity consumption: EIA FAQ — eia.gov/tools/faqs

State-by-state VPP capacity data: explorer.vppcapacity.com

Other Coverage: Latitude Media · Heatmap News · Canary Media · Electrek · Sunrun Press Release